New Freedom With Decentralized Finance (DeFi) – Part II

Previously, decentralized finance (DeFi) was introduced beginning with DeFi platforms with their focus on smart contracts and their blockchain corollaries of traditional finance; then continued with the implementation of DeFi loans; DeFi exchanges with their focus on trading various mintages of cryptocurrencies, e.g., BTC, USDC, USDC, ETH, etc.; payment; remittances; and yield farming, the process […]

New Freedom With Decentralized Finance (DeFi) – Part I

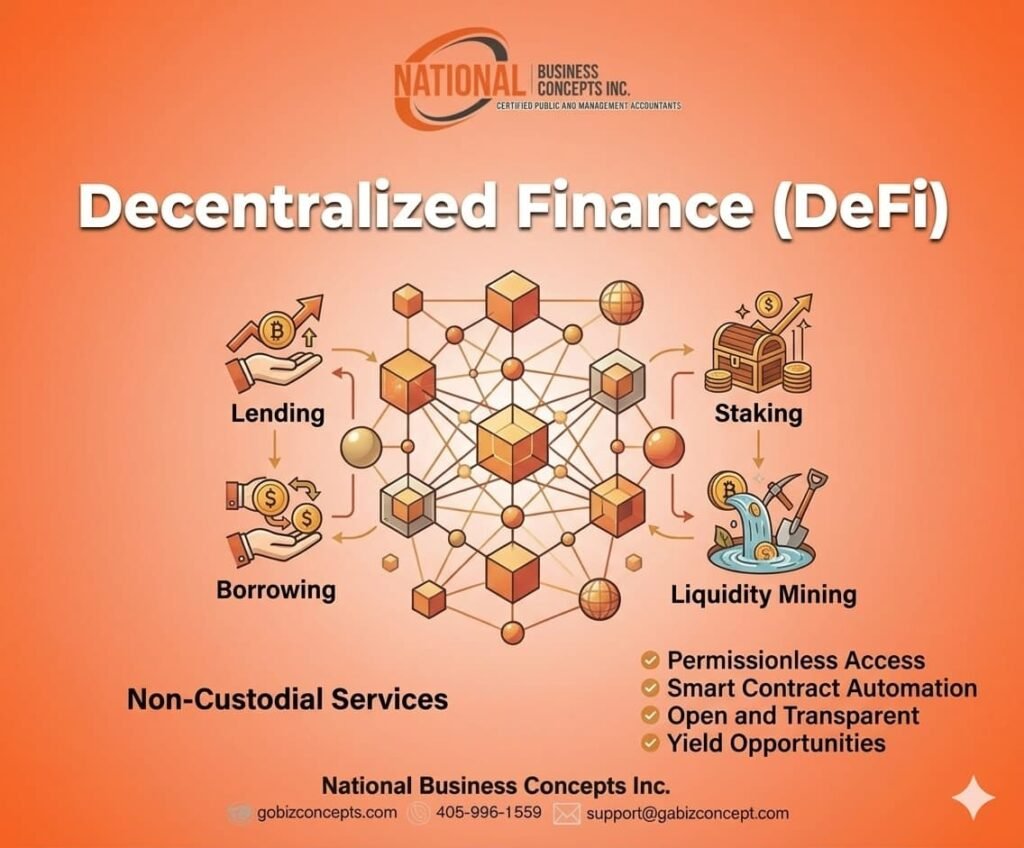

Decentralized Finance (DeFi) has been introduced as a blockchain-based alternative to traditional financial systems, enabling permissionless access to lending, borrowing, trading, and asset management. Cryptocurrency has been utilized as both a medium of exchange and a store of value within this ecosystem, with smart contracts automating transactions and enforcing rules. Loans have been extended through […]

Non-US-Pegged Stablecoins Advantage

As of March 2026, there were about two dozen known, non-US-pegged stablecoins, e.g., EURC / EUROe (Euro) and XSGD (Singapore Dollar). Alternatives to US‑denominated stablecoins, e.g., USDT and USDC, have been increasingly offered as issuers, exchanges, and regulators have sought diversification and resilience. Euro‑backed, yen‑backed, pound‑backed, and regional stablecoins have been introduced by banks, fintech […]

Proven Crypto Stablecoin Redemption to Fiat in The USA

Cryptocurrency stablecoin redemption methods are structured across issuers, exchanges, fintech wallets, and bank partnerships, each shaped by the regulatory framework of the GENIUS Act of 2025. Issuers are mandated to maintain 1:1 reserves in cash or Treasuries, ensuring that redemption requests are honoured at par value. Exchanges are required to enforce know your customer (KYC) […]

Best Use of Crypto Stablecoins For Commerce

Cryptocurrencies, limited coins and stablecoins, are digital or virtual currencies that use cryptography for security and operate on decentralized networks, typically based on blockchain technology. General cryptocurrencies, such as Bitcoin (BTC) and Ethereum (ETH), are known for their volatility and potential for appreciation. They function as both a medium of exchange and a store of […]

Prudent Reckoning Of Changes in Owner’s Equity

Owner’s equity is represented on the balance sheet as the residual interest remaining after liabilities are deducted from assets. It is displayed under the equity section, where capital contributions, retained earnings, and adjustments are summarized to show the owner’s claim on the business. The balance sheet presents this figure at a specific point in time, […]

Clear-cut Difference, Book Value And Market Value

Book Value And Market Value Book value and market value are often contrasted to highlight the difference between accounting records and economic reality. Book value is determined through financial statements, where assets are recorded at historical cost and adjusted for depreciation or impairment. Market value, however, is established by prevailing marketplace conditions, reflecting what buyers […]

Proper Use Of Liquidity, Leverage, & Profitability Financial Ratios Exposed

Financial ratios are widely used as essential tools for evaluating business performance and stability. Liquidity ratios are employed to determine whether short-term obligations can be met through available assets, while leverage ratios are employed to assess the extent of debt financing and the risks associated with long-term solvency. Profitability ratios are utilized to measure the […]

Instructive Focus on Depreciation and Amortization

Depreciation and Amortization Depreciation and amortization are systematic processes used to allocate costs and manage obligations within financial reporting. Depreciation is applied to tangible assets, where value is reduced gradually to reflect usage, wear, or obsolescence over time. Amortization, in contrast, is applied to intangible assets, where costs are spread across useful lives to match […]

How Valuable is Working Capital?

Working Capital The importance of working capital is recognized through its influence on liquidity management, operational efficiency, flexibility and growth, risk management, and cost management. Liquidity is preserved when current assets and liabilities are balanced, ensuring obligations are met without disruption. Operational efficiency is reflected when receivables, payables, and inventory are managed effectively to optimize […]