Title 26 — Comprehensive Codification of The Internal Revenue Code of 1954

The Internal Revenue Code of 1954 was enacted as a comprehensive reorganization of federal tax law, presaged by the Revenue Act of 1939, whose consolidation revealed the necessity of a modern codification. It was legislatively adopted by the 83rd Congress and signed into law to establish Title 26 of the United States Code as the […]

The Internal Revenue Code of 1939 — Simplified

In 1939, the Internal Revenue Code (Revenue Act oof 1939) was enacted to organize scattered tax statutes into a coherent framework. It was defined as the consolidation of permanent and temporary provisions, ensuring clarity and continuity in federal taxation. It traces to the earlier Revenue Acts, particularly of 1862 and 1913, which had established the […]

The U. S. Securities And Exchange Commission — Transparency And Confidence

The U.S. Securities and Exchange Commission (SEC) was established in 1934 under the Securities Exchange Act, when federal oversight was mandated to restore investor confidence after the Great Depression. Central to the regulation of U.S. capital markets, its mission is the protection of investors, importantly, the maintenance of fair and orderly markets, and the facilitation […]

IFRS vs US GAAP Jumpstart Reconciliation

Ongoing convergence between International Financial Reporting Standards (IFRS) and U.S. Generally Accepted Accounting Principles (GAAP), required for companies operating across jurisdictions, is emphasized through reconciliation efforts involving several major standards. Under IFRS 15, revenue is recognized through a principle‑based framework, while ASC 606 codifies similar steps with prescriptive detail. Financial instruments are addressed by IFRS […]

Adaptable International Financial Reporting Standards

International Financial Reporting Standards (IFRS) are a globally recognized framework of accounting principles developed by the International Accounting Standards Board (IASB) and governed by the IFRS Foundation. The standards, established in London, replaced earlier International Accounting Standards (IAS). IFRS is applicable in over 140 jurisdictions, regulating how financial statements are prepared and presented, ensuring transparency, […]

Generally Accepted Accounting Principles For Accounting Clarity

In the United States, Generally Accepted Accounting Principles (GAAP,) a framework of accounting principles, standards, and codes, are applied to regulate how financial statements are prepared and presented, ensuring comparability and reliability across entities. These principles and standards are codified to represent uniform practices that safeguard stakeholders and uphold legal obligations. The Financial Accounting Standards […]

Destiny — Internal Revenue Service

The Internal Revenue Service has been shaped by a long constitutional and legislative history. Its origins were traced to the Commissioner of Internal Revenue and the Bureau of Internal Revenue, both created under the Revenue Act of 1862 to manage Civil War taxation, which included income tax along with tariffs and excise taxes. Permanence was […]

Useful – Network Effect And Viral Effect

The viral effect has been characterized by speed, reach, and cultural cartography, where diffusion is accelerated through social sharing and referral loops. While virality emphasizes exposure, its impact on financial statements may be transient, reflected in revenue spikes or marketing efficiency. Network effects, however, are more likely to be capitalized as goodwill, influencing valuation through […]

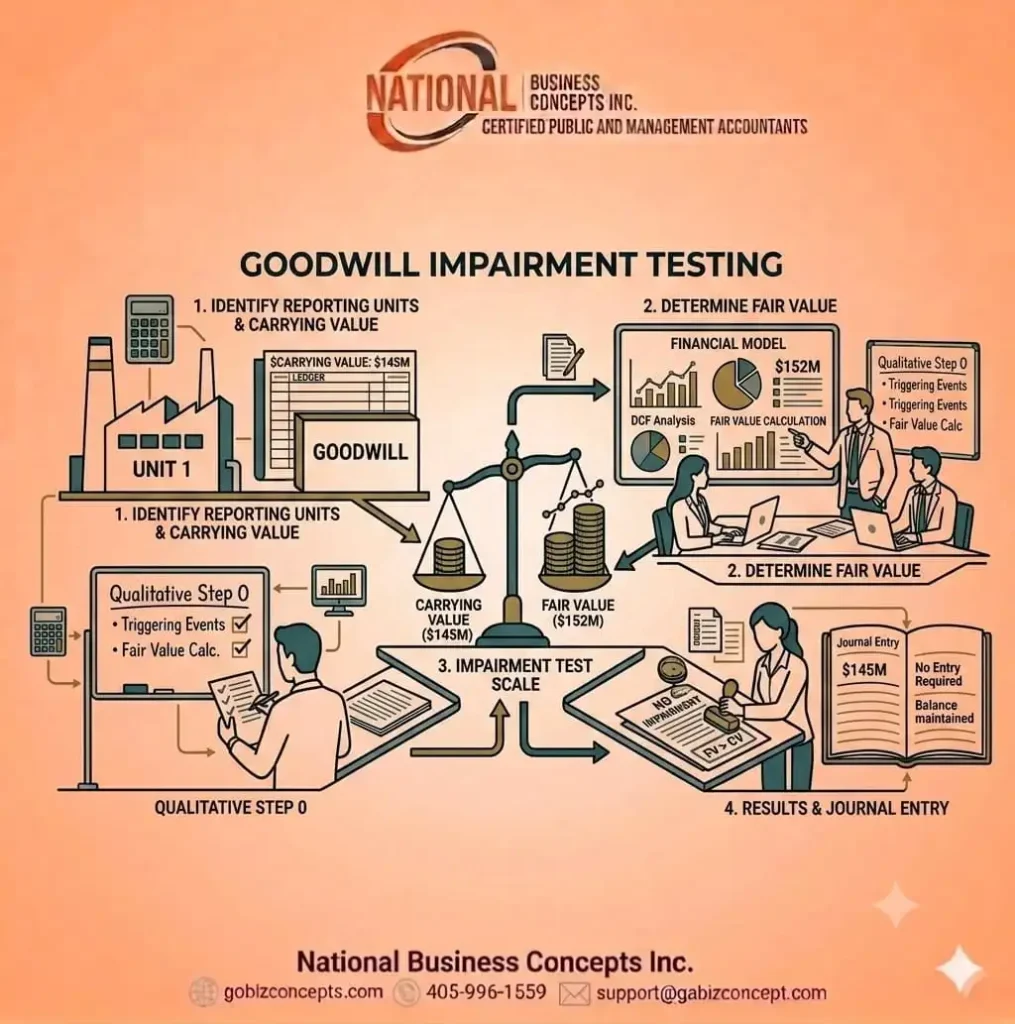

Meticulous Accounting for Goodwill — Impairment Testing

As goodwill is recognized as an intangible asset when acquisition costs exceed the fair value of net assets, goodwill impairment testing is required to ensure its recorded value reflects economic reality. Under accounting standards, goodwill for public companies is never amortized but is subjected to annual reviews or triggered assessments when adverse events occur. The […]

Advantage of The Network Effect as Intangible Asset

In a service business, the institution of the network effect is regarded as a cornerstone for sustainable expansion and competitive resilience. Particularly, the resolution of the “Chicken and Egg” problem is prioritized, for a two-sided marketplace business, since simultaneous attraction of users and providers is required to establish momentum. But in general, distinct network-types manifest, […]