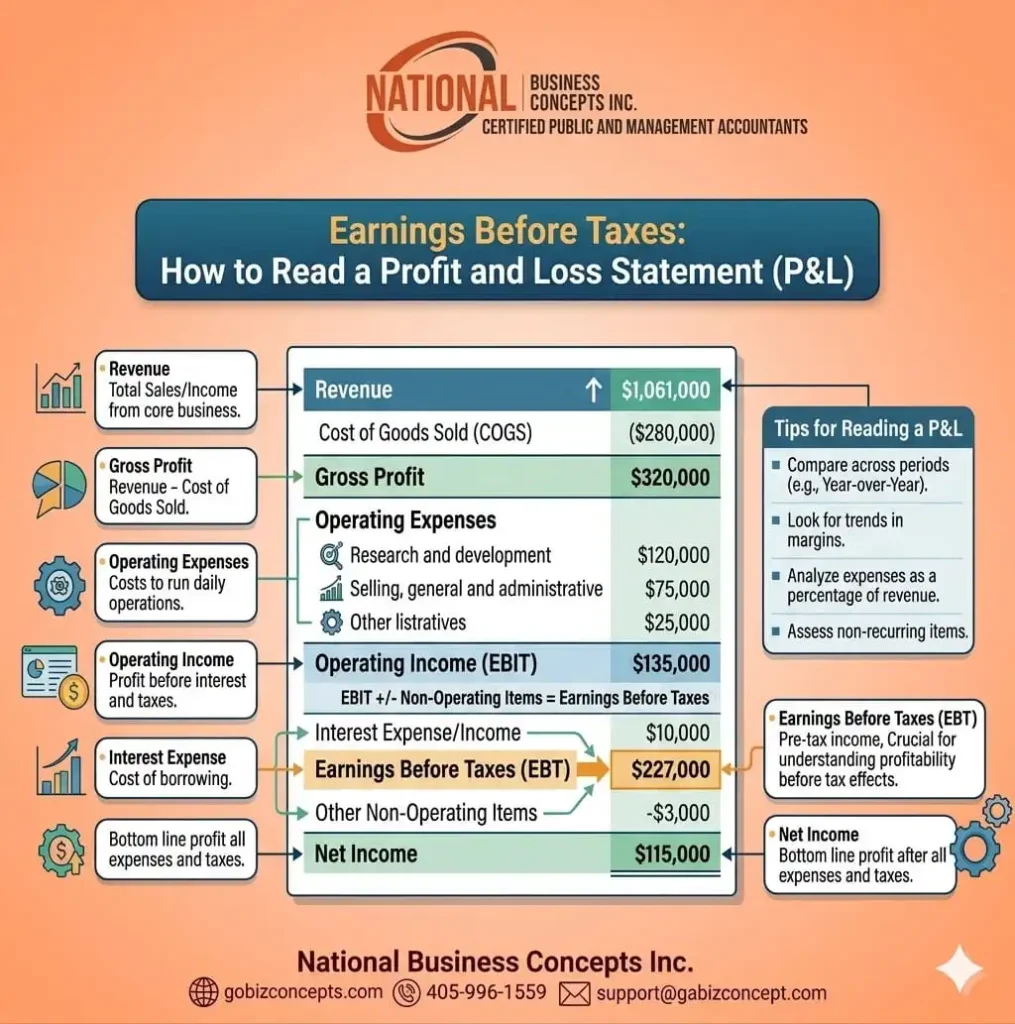

Earnings Before Tax (EBT) is a critical measure of profitability within a Profit and Loss (P&L) Statement, as it reflects income generated before tax obligations are deducted. It is derived after operating income (i.e., earnings before interest and taxes (EBIT)) has been adjusted for interest and other non-operating gains or losses. By isolating tax considerations, EBT provides a clearer view of financial performance that emphasizes both operational efficiency and financing decisions. Its placement within the P&L Statement allows stakeholders to evaluate profitability across companies and industries. Through this measure, insight is offered into how effectively resources are managed, while also preparing the foundation for net income (NI) determination.

EBT Calculation

Earnings Before Taxes is calculated from Earnings Before Interest and Taxes (EBIT) by adjusting for interest-related items and other non-operating gains or losses. EBIT, which represents operating profit before financing and tax considerations, is first reduced by interest expenses incurred on debt obligations. Any interest income earned from investments or cash holdings is then added, along with adjustments for incidental financial activities such as asset sales or foreign exchange gains. Through these modifications, EBT is derived as the measure of profitability prior to taxation, reflecting both operational efficiency and financing decisions. By this calculation, stakeholders are enabled to assess performance without the distortion of tax structures, thereby preparing the foundation for net income determination.

Note on Interest

Interest expense is incurred when funds are borrowed, reflecting the cost of debt financing that reduces earnings available to stakeholders. Conversely, interest income is generated when surplus funds are invested or deposited, representing returns that enhance profitability. Both items are reported below operating income, ensuring that core operations are separated from financing activities.

Non-Operating Gains or Losses

Non-operating gains or losses are financial outcomes that arise from activities outside the core operations of a business. These items are recorded separately from operating income to ensure that the performance of primary operations is not distorted. Gains may be realized through the sale of assets, investment returns, or foreign exchange fluctuations, while losses may occur from asset disposals, litigation costs, or restructuring charges. Their inclusion in financial statements allows Earnings Before Taxes to reflect the impact of incidental or extraordinary events beyond daily operations. By analysing these figures, stakeholders are enabled to assess how external factors influence profitability, thereby gaining a clearer understanding of overall financial stability and risk exposure.

EBIT Determination

EBT calculation is dependent on a successful determination of EBIT. EBIT is a measure of profitability that highlights the performance of a company’s core operations before the influence of financing and tax obligations. It is calculated by subtracting operating expenses, excluding interest and taxes, from total revenue, thereby isolating the efficiency of operational activities. By focusing on operating income, EBIT provides insight into how effectively resources are managed and how sustainable profitability is maintained. This measure is often used by analysts and investors to compare companies across industries, as it eliminates distortions caused by differing tax environments and capital structures. Once more, through EBIT, operational strength is emphasized, forming a basis for subsequent calculations such as EBT and net income.

Earnings Before Taxes Ratios

Financial ratios applicable to Earnings Before Taxes are used to evaluate profitability and efficiency by isolating performance before tax obligations. The EBT margin ratio is calculated by dividing EBT by total revenue, thereby indicating how much profit is retained from sales before taxes are applied. The return on assets ratio can also be derived using EBT, ((EBT+I)/Avg. Total Assets,) showing how effectively assets generate pre-tax earnings. Additionally, the interest coverage ratio ((EBT + Interest Expense)/Interest Expense) highlights the ability of earnings to cover interest expenses, reinforcing financial stability. These ratios allow comparisons across companies and industries, again, without distortion from differing tax structures, enabling stakeholders to assess operational efficiency, financing decisions, and overall profitability in a consistent manner.

IRS Looks at EBT

Earnings Before Taxes is considered important to the Internal Revenue Service (IRS) because it serves as the foundation upon which tax liabilities are assessed. By isolating income before taxes, EBT provides a standardized measure of profitability that ensures consistency in evaluating taxable earnings across different companies and industries. The IRS is able to determine the amount of income subject to taxation without distortion from varying accounting treatments of tax expenses. Through EBT, transparency in financial reporting is enhanced, enabling accurate enforcement of tax regulations and compliance monitoring. This measure ensures that the IRS can fairly apply tax codes, verify reported income, and safeguard government revenue derived from corporate and business activities.

Relation of EBT to Net Income

Earnings Before Taxes is directly related to net income, as it serves as the immediate precursor in the Profit and Loss Statement. Once EBT has been determined by adjusting operating income for interest expenses, interest income, and non-operating gains or losses, tax obligations are subtracted to arrive at net income. This relationship highlights how profitability before taxes is transformed into the final measure of earnings available to shareholders. By isolating EBT, the impact of taxation can be clearly observed, allowing stakeholders to evaluate how government levies affect overall financial performance. Net income is therefore dependent on EBT, with the latter providing the foundation upon which tax liabilities are applied, and final profitability is established.

Conclusion

Earnings Before Taxes is a key profitability measure in the Profit and Loss Statement, derived from Earnings Before Interest and Taxes (EBIT) by adjusting for interest expenses, interest income, and non-operating gains or losses. EBIT highlights operational performance by subtracting operating expenses, excluding interest and taxes, from revenue. EBT ratios, such as margin and return on assets, are used to evaluate efficiency before tax obligations. The IRS relies on EBT to assess taxable income consistently across companies. Finally, EBT directly precedes net income, as tax obligations are subtracted from it to determine final earnings available to shareholders, making it essential for both financial analysis and regulatory compliance.

Richard Thomas