As goodwill is recognized as an intangible asset when acquisition costs exceed the fair value of net assets, goodwill impairment testing is required to ensure its recorded value reflects economic reality. Under accounting standards, goodwill for public companies is never amortized but is subjected to annual reviews or triggered assessments when adverse events occur. The carrying amount is compared with fair value, and any excess is recorded as an impairment loss. This adjustment prevents overstated asset values and maintains transparency for stakeholders. By enforcing systematic evaluation, impairment testing safeguards the reliability of reported earnings and ensures financial statements remain aligned with prevailing market conditions and organizational performance.

Impairment Testing Requirement

Impairment testing for goodwill is required under both Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS,) to ensure that recorded values remain consistent with economic reality. Under GAAP, public companies must perform annual impairment tests at the reporting unit level, with additional assessments triggered by adverse events such as declining cash flows or market downturns. Private companies may elect to amortize goodwill over a period not exceeding ten years, thereby reducing the need for annual testing. Under IFRS, goodwill is never amortized and must always be tested for impairment at the cash-generating unit level. If the carrying amount exceeds recoverable value, an impairment loss is recognized, reducing both goodwill and earnings.

Impairment Testing Amortization Exception

Under GAAP, amortization of goodwill for private companies is permitted as an alternative to annual impairment testing, thereby reducing the cost and complexity of compliance. Goodwill is amortized on a straight-line basis over a period not exceeding ten years, unless a shorter useful life can be justified. This election allows private entities to systematically reduce goodwill over time, reflecting the gradual decline of intangible benefits associated with acquisitions. Although impairment testing is still required when triggering events occur, the amortization option provides a predictable expense pattern and simplifies reporting obligations. By enabling this approach, GAAP ensures that smaller, closely held businesses can maintain reliable financial statements without incurring the burdens of complex valuation procedures.

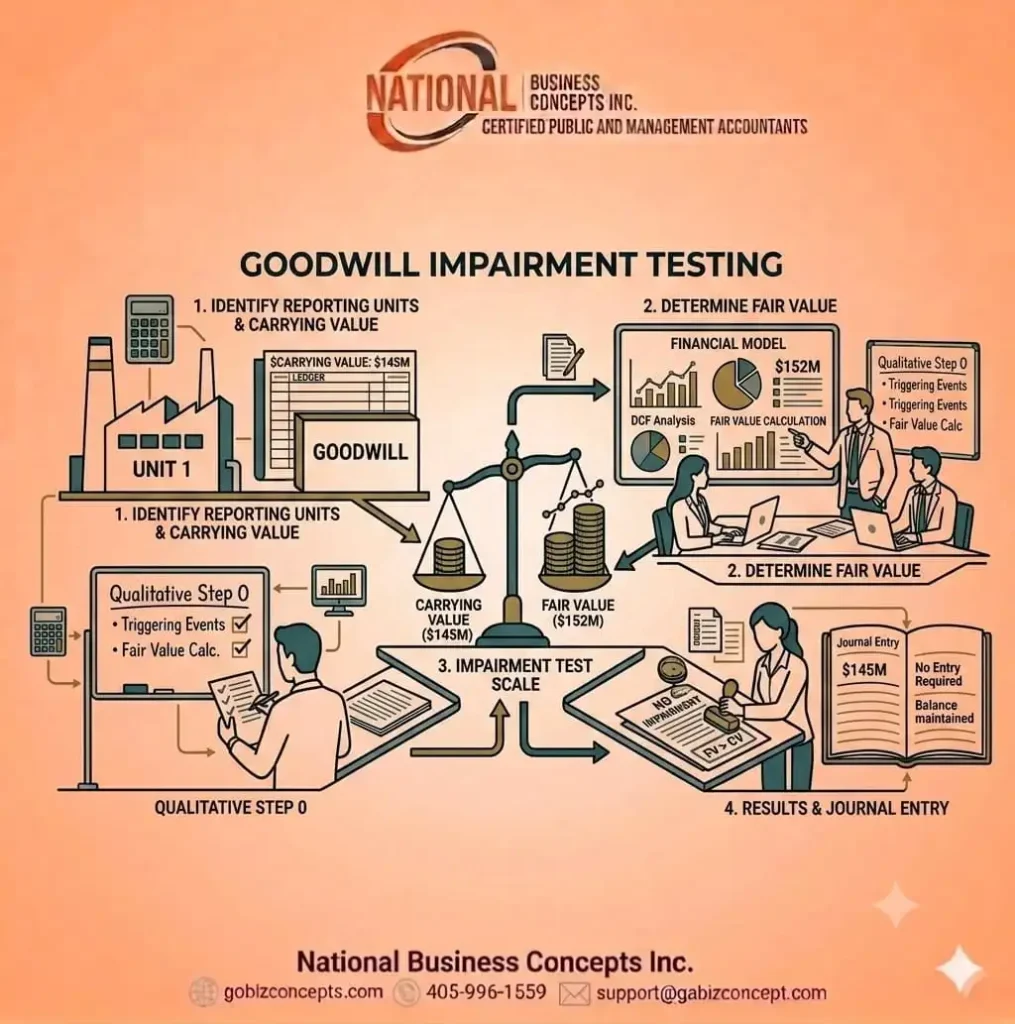

Fair Value Assessment Methods

Fair value assessment methods for goodwill impairment are applied through both qualitative and quantitative approaches to determine whether carrying amounts, based on the overall value of the reporting unit, exceed recoverable values. In qualitative assessments, factors such as market conditions, industry trends, and management outlook are evaluated to identify potential impairment indicators without detailed calculations. When quantitative testing is required, valuation techniques such as discounted cash flow (DCF), comparable company analysis, and market multiples are employed. DCF involves projecting future cash flows and discounting them to present value, while comparable company analysis benchmarks performance against peers. Market multiples rely on valuation ratios derived from similar transactions. These methods ensure that goodwill values remain aligned with economic value.

Impairment Annual Testing and Triggering Events

As stressed before, under both GAAP and IFRS, goodwill must be tested at least once each year, typically at a chosen date such as the end of the fiscal year. In addition to this scheduled review, impairment testing is triggered by specific events that indicate potential declines in value. Such events include deteriorating economic conditions, adverse regulatory changes, declining cash flows, or significant market competition. When these circumstances arise, the fair value of the reporting unit or cash-generating unit is reassessed against its carrying amount. If impairment is identified, a loss is recognized, thereby ensuring transparency, accuracy, and reliability in financial reporting.

Identifying Reporting Unit

Identifying reporting units for impairment testing must be carried out to ensure that goodwill is assessed at the appropriate organizational level. Under GAAP, reporting units are defined as operating segments or components of segments that have discrete financial information and are regularly reviewed by management. These units must be capable of generating independent cash flows and must be aligned with how the business is managed internally. The allocation of goodwill to reporting units is performed at acquisition, and subsequent impairment testing is conducted at this level to capture changes in fair value. By requiring goodwill to be tested at the reporting unit level, accounting standards ensure that impairments are recognized where economic declines occur.

Impairment Calculation

Impairment loss calculation is performed by comparing the carrying amount of goodwill with its fair value, and recognition is required when the carrying amount exceeds recoverable value. Under both GAAP and IFRS, the process begins with the estimation of the fair value of a target unit through methods such as discounted cash flow, market multiples, or comparable company analysis. Once fair value is determined, it is subtracted from the carrying amount of goodwill to identify the impairment loss.

For example, if Company B was purchased by Company A for $370 million, which included $100 million recorded as goodwill. Following a decline in overall business value, the fair value of Company B was reassessed at $300 million. To calculate the impairment loss, the carrying amount of goodwill is compared with the revised fair value. Since goodwill was initially valued at $100 million and the reassessment reduced the total firm value, goodwill is determined to have fallen to $30 million. The impairment loss is therefore $100 million – $30 million = $70 million.

Impact on Ledger Accounts and Financials

For our impairment calculation example, ledger accounts are adjusted by recording the impairment loss as an expense and reducing the goodwill account. The entry is posted by debiting the impairment loss account for $70 million and crediting the goodwill account for the same amount, thereby reflecting the decline in value. On the financial statements, the impairment loss is presented in the income statement as a non-cash expense, which reduces net income. Simultaneously, the balance sheet shows goodwill reduced from $100 million to $30 million, ensuring assets are not overstated. This adjustment aligns reported values with economic reality, maintains transparency, and provides stakeholders with reliable information about the company’s financial position and performance.

Conclusion

Goodwill is recognized as an intangible asset when acquisition costs exceed the fair value of net assets, and impairment testing is required to ensure accuracy. Under both GAAP and IFRS, goodwill must be tested annually, with additional reviews triggered by adverse events. Private companies under GAAP may elect to amortize goodwill over a period not exceeding ten years, reducing compliance complexity. Fair value assessments are conducted using qualitative and quantitative methods, including discounted cash flow, comparable company analysis, or market multiples. Reporting units must be identified to allocate goodwill appropriately, and impairment losses are calculated when carrying amounts exceed recoverable values. These requirements safeguard transparency, prevent overstated assets, and ensure financial statements reflect economic reality.

By Richard Thomas