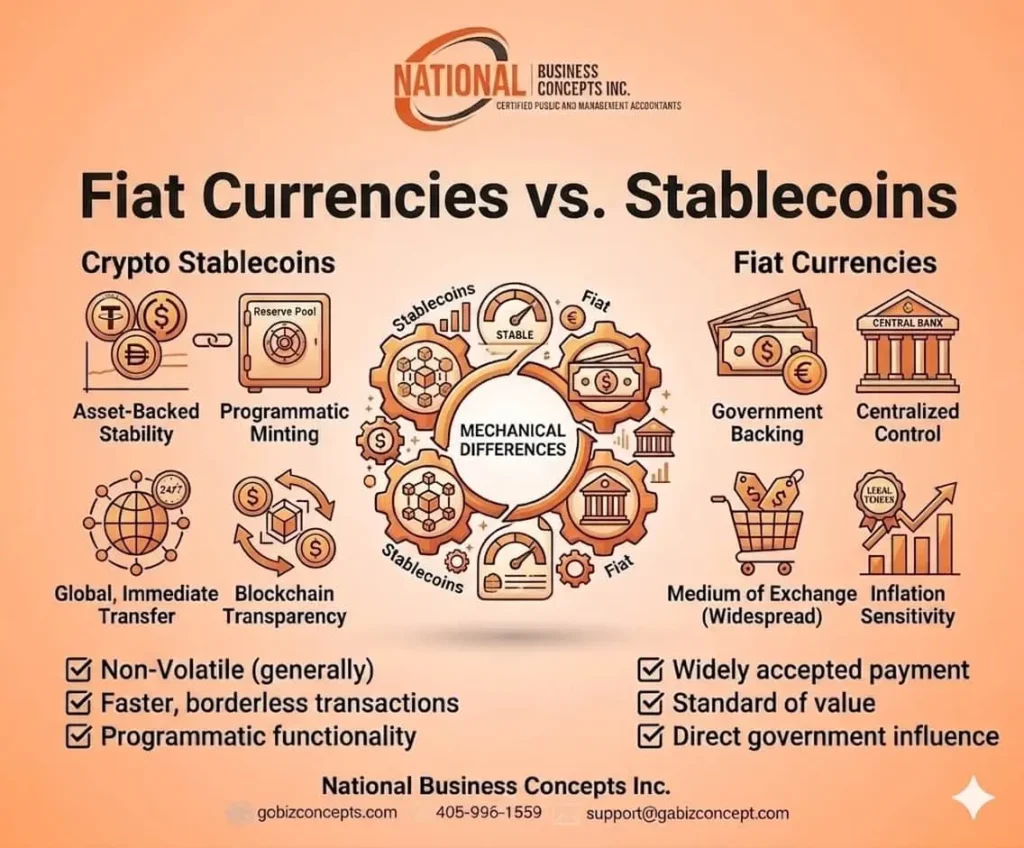

Essentially, fiat Currencies and stablecoins are contrasted through their issuers, legal recognition, and operational frameworks. Fiat currencies, such as the U.S. dollar, are issued by governments and central banks, recognized as legal tender, and backed by national authority. Crypto stablecoins, including USDT and USDC, are issued by private entities, pegged to fiat reserves, and regulated as digital assets rather than legal tender. Shouldering in, like the proposed US digital dollar, are Central Bank Digital Currencies (CBDCs) merging governmental authority with blockchain efficiency. Transaction use differs, with fiat dominating everyday commerce and stablecoins facilitating digital finance. Speed and cost favour crypto stablecoins in cross-border transfers, while volatility remains low with adequate reserves. Regulation is strict for fiat and evolving for stablecoins.

Issuers/Institutional Backing

Fiat Currencies and stablecoins are distinguished primarily by their issuers / backers. Fiat currencies, such as the U.S. dollar, are issued by governments and central banks, with authority derived from national legislation and value sustained by sovereign credibility, fiscal and monetary policy, and economic strength. Stablecoins, including USDT and USDC, are issued by private companies or decentralized protocols, with value pegged to fiat reserves or equivalent assets, e.g., government securities. CBDCs, i.e., digital fiat, combine governmental authority with digital infrastructure and efficiency. Trust in fiat is maintained through sovereign backing, while stablecoins rely on transparency of reserves and issuer credibility. Thus, the type of issuer defines legitimacy, regulation, and acceptance across both traditional and digital financial systems.

Take note, CBDCs are being developed and launched in disparate places as sovereign-backed digital money. The Sand Dollar in the Bahamas was introduced in 2020 as the first retail CBDC, while Nigeria’s eNaira and Jamaica’s JAM-DEX were launched to enhance financial inclusion and payment efficiency. China’s Digital Yuan (e-CNY) is undergoing large-scale pilot programs, and the Eastern Caribbean’s DCash serves multiple island nations. In Europe, the Digital Euro is being tested, and Canada has explored wholesale CBDCs through Project Jasper. The proposed U.S. Digital Dollar remains in the research stage, intended to merge fiat legitimacy with blockchain efficiency. These examples demonstrate how CBDCs are reshaping monetary systems globally. Disparate

Legal Status

The legal statuses of fiat currencies and stablecoins are defined by distinct frameworks of recognition and authority. Fiat currencies, such as the U.S. dollar, are designated as legal tender, mandated for the settlement of debts, taxes, and official transactions under government regulation. Stablecoins, including USDT and USDC, are not granted legal tender status; instead, they are classified as digital assets and subjected to evolving regulatory oversight. As stated before, their legitimacy is dependent on issuer transparency and reserve audits rather than sovereign backing. CBDCs have full legal status, as they combine governmental authority with digital efficiency. Thus, fiat enjoys universal enforceability, while stablecoins remain conditionally recognized within financial systems.

Regulation

Legal frameworks of recognition and authority provide for the regulation of stablecoins and fiat currencies. Fiat currencies, such as the U.S. dollar, are strictly regulated by governments and central banks, with monetary policy, banking laws, and financial oversight ensuring stability and legitimacy. Stablecoins, including USDT and USDC, are subjected to evolving regulatory measures, classified as digital assets rather than legal tender, and monitored, as said before, for reserve transparency, consumer protection, money laundering, and systemic risk. CBDCs are regulated directly under sovereign authority, merging fiat legitimacy with blockchain efficiency. Thus, fiat regulation is comprehensive and established, while stablecoin regulation remains adaptive, fragmented, and dependent on issuer compliance with emerging standards.

Transactional Use

Transaction use highlights clear, but evolving, differences between stablecoins and fiat currencies. Fiat currencies, such as the U.S. dollar, are used, typically, in everyday commerce, wages, taxes, and debt settlement, with transactions processed through banks, payment networks, and regulated financial institutions. Stablecoins, including USDT and USDC, are primarily used in digital finance (DeFi), cryptocurrency exchanges, remittances, growing commercial transactions, as efficient payment solutions for outsourcing, independent contracting, the gig economy, and on decentralized platforms, with transfers executed on blockchains rather than through traditional intermediaries.

Speed and Cost

Speed and cost in transactions are differentiated between fiat currencies and stablecoins by the mechanisms through which payments are processed. Fiat currencies, such as the U.S. dollar, are transacted through banks, payment networks, and international clearing systems, with cross-border transfers often slowed by intermediaries and burdened by fees. Stablecoins, including USDT and USDC, are transacted on blockchain networks, where transfers are executed rapidly and at lower cost, particularly across borders. CBDCs, combining fiat legitimacy with blockchain efficiency, reduce settlement delays and transaction expenses under government oversight. Thus, fiat transactions are characterized by higher costs and slower speeds, while stablecoins offer faster, cheaper alternatives within digital ecosystems.

Volatility

Volatility is experienced differently between Fiat Currencies and Stablecoins due to the mechanisms through which value is maintained. Fiat currencies, such as the U.S. dollar, are stabilized by government authority, fiscal and monetary policy, and central bank interventions, with fluctuations generally limited to inflationary pressures or exchange rate shifts. Stablecoins, including USDT and USDC, minimize volatility by being pegged to fiat reserves, though risks arise if reserves are mismanaged or transparency is lacking. CBDCs combine fiat stability with digital infrastructure and efficiency, ensuring minimal volatility under sovereign oversight. So, fiat stability is institutionally enforced, while stablecoin stability is conditionally dependent on issuer credibility and reserve integrity.

Conclusion

Concluding, fiat currencies and stablecoins, and CBDCs differ in issuers, recognition, and stability. Fiat currencies like the U.S. dollar are issued by governments and central banks, recognized as legal tender, and backed by sovereign authority. Stablecoins such as USDT and USDC are issued by private entities, pegged to fiat reserves, and regulated as digital assets rather than legal tender. CBDCs, including the proposed digital dollar, are designed to merge governmental authority with blockchain efficiency. Transaction use, speed, cost, and volatility vary, with fiat supported by established regulation, stablecoins reliant on issuer credibility, and CBDCs intended to provide sovereign-backed digital stability.

NB: This article is for informational purposes only and does not pretend to give investment or financial advice.

By Richard Thomas